2021 2nd Quarter Update

Top Headline for Q2: Continued Rotation with Rising Fed Dependency

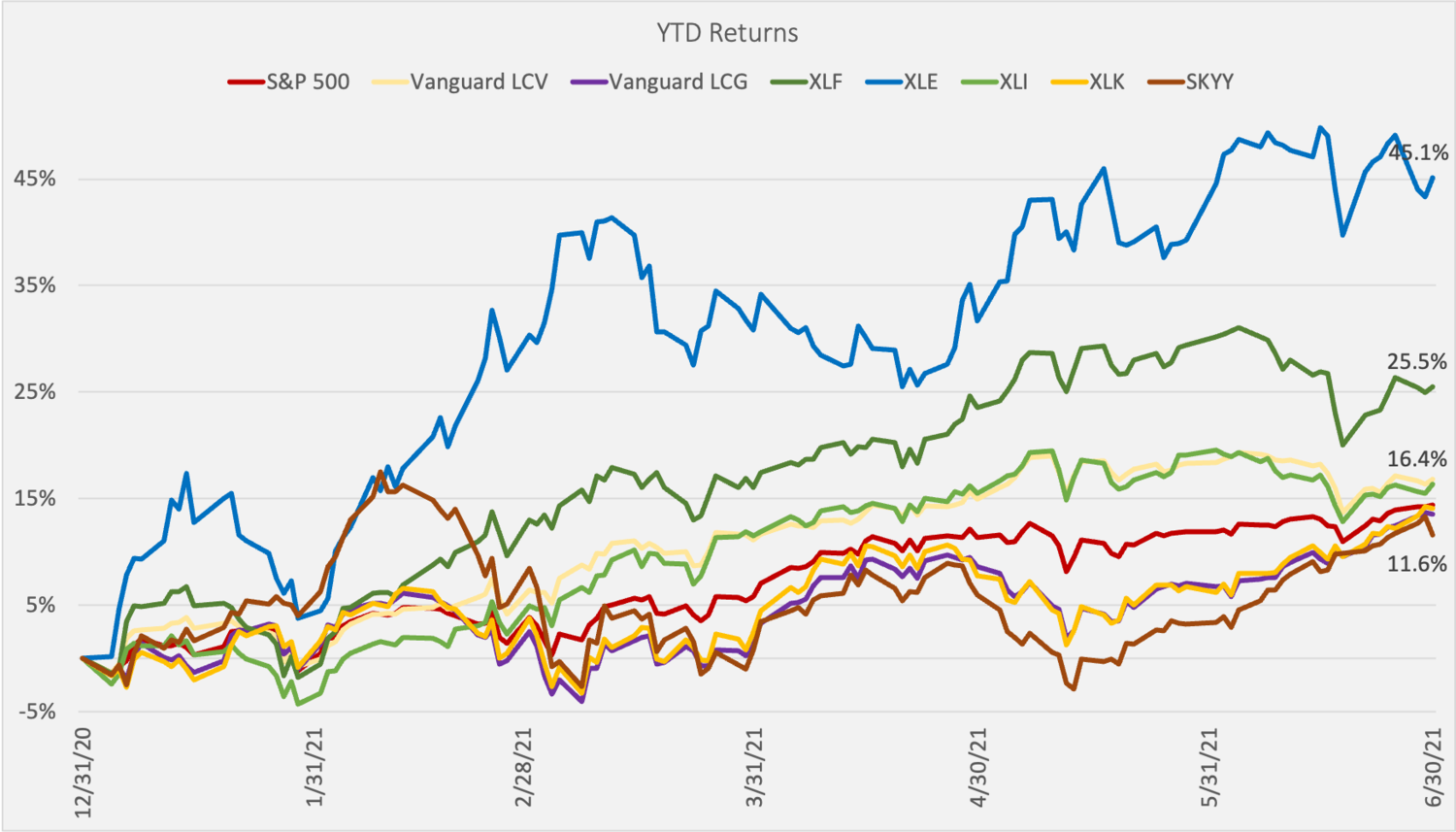

In some ways the second quarter was a continuation of the first. Value trades continued to perform well with more economically sensitive sectors like energy, financials, and industrials pushing higher. Energy proved to be the top performer year-to-date with XLE up 45.1% through June 30th. However, it’s also noteworthy that all equity sectors performed well. The overall stock market has now been up for 6 months in a row, 5 quarters in a row and it seems to be making new all-time highs on a weekly basis. It’s becoming more and more clear that Federal Reserve Bank actions are having a massive impact on markets. The increased liquidity and interest rate impact from the continued $120 billion in monthly bond buying, along with guidance surrounding interest rates, is proving to be a massive tailwind for risk assets.

General Market Update

US Equities: The S&P 500 Index finished up 8.2% for the quarter and the Nasdaq Composite was up 9.5%. The Russell 2000 small cap index lagged a bit – rising “only” 4.1%. Growth made a late 2nd quarter comeback, benefiting from a drop in yields during the quarter. The Vanguard Large Cap Growth ETF (VUG) ended the quarter up 11.7% while its Value counterpart, Vanguard Large Cap Value (VTV) was up 5.1%. Two other notable 2nd quarter “comebacks” were the Technology (XLK) sector, which was up 11.4% in 2Q after only being up 2.4% in 1Q, and Cloud Computing (SKYY), which was up 10.7% in 2Q after being up 0.8% in 1Q. Despite this Growth comeback, several Value subsectors, which Patina Wealth portfolios have exposure to, performed well during Q2. Energy (XLE) ended Q2 up 10.9%, putting it up 45.1% YTD and Financials (XLF) ended Q2 up 8.2%, putting it up 25.5% YTD. The stock market is clicking on all cylinders at this point benefitting from a number of tailwinds including fiscal and monetary support from the federal government and continued good news related to the COVID-19 virus in the United States.

Data Source: Yahoo Finance

International and Emerging Market Equities: The Schwab International Equity ETF, which holds stocks of developed markets excluding the United States, was up 4.9% in Q2 and the Schwab Emerging Markets ETF was up 3.5%. The international market has lagged US indices in recent quarters likely due to better news on the US COVID front, including increased vaccine penetration and general reopening optimism. Emerging markets continue to have attractive relative valuations but the emergence of COVID variants is a greater threat in the sector and will likely limit growth for a bit longer. For example, the daily COVID numbers in India has subsided but saw a substantial spike during Q2.

Fixed Income and Credit: The 2nd quarter was an interesting one for the bond market. After a very rough first quarter where bond prices tanked on “re-opening” optimism, rates tended to trend downward in Q2 as bond prices generally rose. After seeing the 10-year treasury bond yield rise from 0.92% to 1.75% during the 1st quarter, it fell back down to 1.44% by the end of Q2. This was a bit of an unusual move as the equity market optimism and inflation talk would normally lead to falling bond prices and rising yields. It’s possible that Q1 may have been an overshoot of inflation expectations leading to a short-term decline in Q2.

Data Source: Yahoo Finance

Commodities and Precious Metals: Many commodities continued to rise during the quarter as supply chain issues resolve slowly. It remains unclear whether some of these price movements will prove “transitory” as indicated by the Federal Reserve Bank. Precious metals continue to trend sideways as uncertainty persists on the inflation front and risk assets continue to perform well, offering an attractive alternative. Real yields continue to be negative which would normally be a bullish environment for precious metals but the relentless rise in risk assets is limiting investment flows into the category.

A Look Ahead

It feels like we’re getting near the end of the easy money policies from the Federal Reserve Bank. They’ve indicated that they are not likely to raise rates for quite some time but they also indicated that a tapering of their bond buying may be in the cards for the 2nd half of 2021. It’s tough to tell (1) if they’re going to follow through on this action and (2) if so, what impact it will have on markets. Using the last 10 years as a guide, the stock market will not react favorably to any tapering or talk of raising interest rates so it’s important to watch Fed actions closely.

It’s also noteworthy that political pressures are building that could adversely impact equity markets in the long-term. For example, there is further discussion around increased corporate taxation, increased minimum wage, and a general disdain for a rising “wealth gap” that could lead to policies disadvantageous to large businesses. There is also a renewed call for updating of the anti-monopoly policies which could threaten the FAANG complex and other large cap companies.

It would not be surprising to see some increased volatility in the coming quarter. It’s not normal for equity markets to go up in a straight line and we’re long overdue for a pull back. However, the overall landscape is still very favorable to stocks and we’d view any pull back as an opportunity. Rock bottom interest rates, continued Federal Reserve Bank bond buying, aggressive federal government spending packages and a slow-moving congressional process suggests a bright near-term future for equities. Plus, COVID news continues to be positive and consumer enthusiasm is strong, leading to what will likely be historic GDP growth.

So, where does the rubber hit the road? You can’t get something for nothing and it’s clear that as a nation we’re spending money we don’t have. That is, we’re running massive deficits leading to record federal debt levels and increasing the money supply/devaluing the currency to deal with it. One would expect this environment to be inflationary. Clearly, we’re seeing inflation in some areas (e.g., risk assets, home prices, car prices, etc.). Our bet is that, in the long term, asset inflation is the path out of the current debt dilemma for Federal Banks. That is, there is no obvious path to paying down the debt through austerity so it’s likely that federal policy will allow inflation to rise well above prevailing interest rates in an effort to deflate the relative size of the debt. This tactic may also involve continued bond buying as a form of “yield curve control” to ensure that interest rates (aka debt costs) do not grow to an unsustainable level. Given this backdrop, real assets and precious metals will likely see renewed interest as an investment when/if equity markets cool down a bit.